AI training clusters now require massive parallel communication across thousands of GPUs. The GPU-to-optics ratio has escalated from 1:3 (H100) to 1:4.5 (B300) and up to 1:8 for custom ASICs . Traditional pluggable modules cannot keep pace with this demand.

OSFP modules max out at ~51.2Tbps per rack unit. XPO delivers 204.8Tbps per OCP rack unit—4× the density , enabling AI clusters to scale without expanding physical footprint.

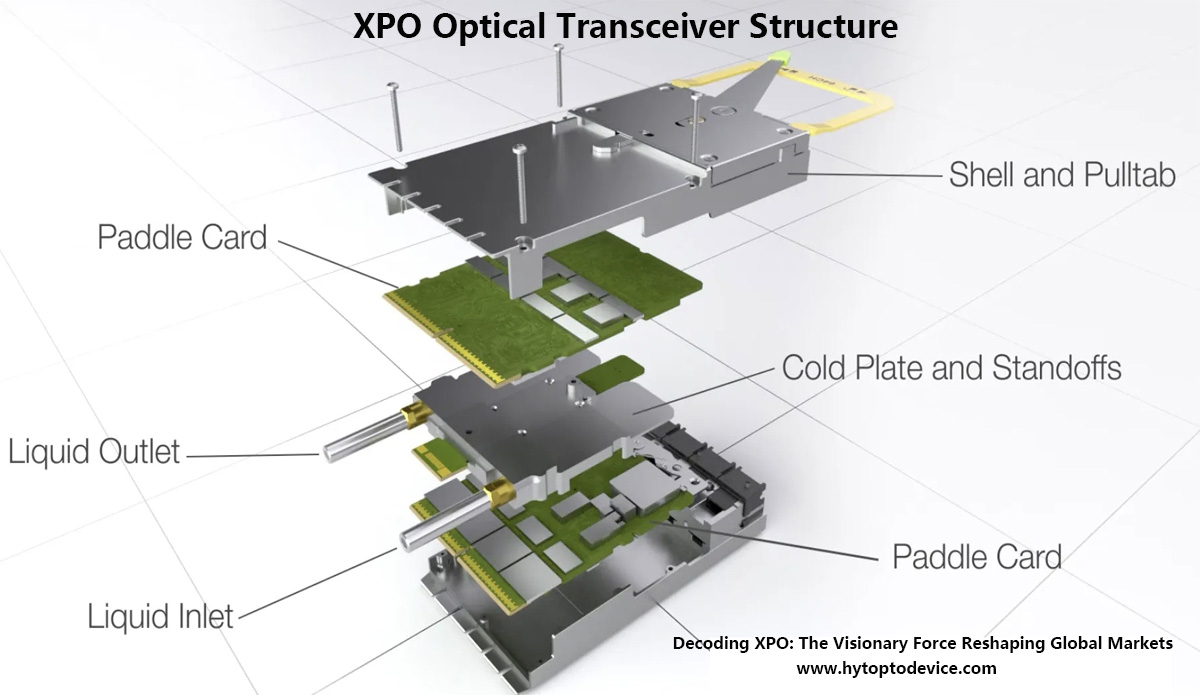

With GPU power exceeding 1000W, liquid cooling is now essential. XPO is the first pluggable standard with integrated liquid cooling, dissipating up to 400W per module —a 20× increase over air-cooled transceivers .

March 2026: Arista leads formation of XPO MSA with 45 industry partners , including Lightmatter, TeraHop (InnoLight), and Eoptolink . ChineseTeraHop and Eoptolink will demonstrate the first 12.8Tbps XPO module at OFC 2026 .

1.5 The Unstoppable Rise of XPO: A Masterclass in Market Disruption

The XPO emerged to address system challenges arising from AI fabric bandwidth constraints, limited front panel space, continuously rising module power consumption, and the practical limitations of liquid cooling. It attempts to rebalance density, thermal design, reliability, and maintainability, upgrading pluggable to a new level: higher density, higher power consumption, liquid cooling support, while still retaining front panel pluggability and serviceability.

| Feature | XPO | NPO | CPO |

| Optics Location | Front-panel pluggable | On PCB near ASIC | Inside ASIC package |

| Integration Level | Module-level | Board-level | Die-level |

| Serviceability | Hot-swappable | Often socketed | Permanent |

| Thermal Management | Integrated liquid (400W) | Board-level | Package-level |

| Bandwidth/Module | 12.8Tbps | Varies | Varies |

| Rack Density | 204.8Tbps/OU | High | Highest |

| Interface Options | Linear/Half/Full | Varies | Limited |

| Time to Market | 2026-2028 | 2026-2029 | 2028+ |

XPO: Fully hot-swappable—field replacement without switch downtime,low maintenance cost

NPO: Often socketed, replaceable but requires more effort,high maintenance cost

CPO: Permanent integration—failed optics require replacing entire assembly,Low maintenance cost,extremely high maintenance costs

XPO's integrated liquid cooling is a game-changer:

400W dissipation capacity vs. 15-25W for air-cooled modules

15-20°C lower component temperatures

Every 10°C reduction approximately doubles component lifetime

XPO: Higher absolute power but 4× density improves power/bit. Supports LPO for additional savings

NPO: Improved efficiency over pluggables (shorter electrical traces)

CPO: Ultimate theoretical efficiency (minimal electrical distance)

Cost dynamics:

2026-2027: XPO commands premium pricing

2027+: Volume economics drive cost-per-bit below alternatives

System-level savings (reduced switches, cabling, rack space) offset module premiums

March 2026: XPO MSA announced with 45 partners

OFC 2026: ChineseTeraHop and Eoptolink demonstrates first 12.8Tbps XPO 8×DR8 module

Specification development, interoperability testing, early sampling

Initial production from multiple suppliers

Deployment in select hyperscale AI clusters

Reliability validation, supply chain qualification

Cost reduction through yield improvements

Multi-million unit annual production

Cost-per-bit parity with alternatives

Second-generation modules, broader ecosystem

Silicon photonics maturity enables scale

Silicon photonics enabler:

Innolight: 95% yield on SiPh chips

TFC Communication: 90% yield on 1.6T SiPh engines

Laser Chip Constraints:

EML chips critical for 200G/lane

Chinese manufacturers scaling: ~1B units 2026, 3B projected 2027

Customer qualification cycles exceed 1 year—high barriers to entry

DSP Availability:

XPO's LPO support reduces DSP dependency

Linear interfaces offer 30-50% power savings

MEMS Components:

Critical for Google's Apollo OCS architecture

Lumentum supply directly influences deployment pace

AI Investment Scale:

Allianz Research: AI investments reach $571 billion in 2026

Optical spending as % of cloud capex: 2.7% (2025) → 3.1% (2026) → 4.1% (2031)

Uncertainties:

Will AI investment sustain current pace?

Could model efficiency reduce compute requirements?

Inference vs. training mix affects optical needs

Historical Patterns:

40%+ annual price erosion for mature products

Premium phase for new generations (12-18 months)

XPO Price Trajectory:

| Period | Premium vs. Alternatives |

|---|---|

| 2026-2027 | Significant |

| 2028 | 1.5-2× |

| 2029+ | Parity or better on cost-per-bit |

Google Ironwood + Apollo OCS:

3D Torus topology for low-latency GPU communication

Apollo OCS: all-optical inter-rack network

95% power reduction vs. traditional switches

From Component to Core Infrastructure:

Optical modules now strategic enablers of AI performance

Capital expenditure allocation growing accordingly

NPO (Near-Packaged Optics) :

Optics on PCB near ASIC, often socketed

Improved signal integrity, better serviceability than CPO

Projected 48% market share

CPO (Co-Packaged Optics) :

Optics inside ASIC package, permanent

Ultimate efficiency, maximum density

Challenges: thermal management, yield, serviceability

Projected 34% market share

LPO (Linear-drive Pluggable Optics) :

Removes DSP, drives laser directly

30-50% power reduction, lower latency

Supported within XPO's flexible architecture

Global AI Investment Cycle:

$571 billion in 2026—largest tech investment cycle ever observed

Much invested in tangible assets: buildings, servers, power, cooling

Data Center Power Constraints:

IEA: Global data center electricity could nearly double by 2030

~1,000 terawatt-hours (~3% of global demand)

Single rack exceeding 100kW

Power availability becomes primary expansion constraint

Energy Efficiency as Advantage:

Google Apollo OCS: 95% power reduction

XPO integrated cooling + LPO support contribute to efficiency goals

| Technology | Role |

|---|---|

| XPO | Ultra-density with serviceability (4× OSFP density, integrated liquid cooling) |

| NPO | Pragmatic middle ground (board-level integration, socketed optics) |

| CPO | Long-term integration vision (ultimate efficiency, permanent) |

Key takeaways:

XPO delivers 12.8Tbps/module, 204.8Tbps/OU, 400W liquid cooling

Removable optics (XPO/LPO/NPO) represent 68% of market with 1:7.7 GPU attach ratio

Power and density are the new battlegrounds—energy-efficient, high-density solutions win

Standardization accelerating: 5 major MSAs launched March 2026, XPO MSA with 45 partners

The terabit era has arrived. Multiple architectures will shape its evolution.

At HYTOPTODEVICE, we combine decades of optical manufacturing expertise with cutting-edge innovation.

True Source Factory:

In-house component packaging and optical assembly

Rigorous quality testing across temperature ranges

Direct supply chain management

Rapid prototyping and custom design

Technology Leadership:

Active tracking of XPO, NPO, CPO, LPO developments

Roadmap aligned with evolving customer requirements

Quality Commitment:

100% full-temperature testing

BER validation

Environmental stress screening

Long-term reliability verification

Global Support:

Application engineering assistance

Custom design services

Global logistics

Rapid field response

Whether you're planning for XPO deployment in 2027 or need high-performance modules today, HYTOPTODEVICE is your trusted partner.

7.Frequently Asked Questions (FAQs)

7.1.Q:Who is supporting the XPO MSA?

A:The XPO MSA is led by Arista with 45 industry partners, including Lightmatter, TeraHop (InnoLight), and Eoptolink

7.2.Q:How does XPO address thermal challenges?

A:The XPO pluggable module comes with an integrated liquid cooling plate that can dissipate up to 400W of heat per module, that will enable it to operate in a liquid-cooled AI rack.

7.3.Q:Which technology offers the best serviceability?

A:XPO modules support hot-swapping, offering optimal maintainability. NPO modules typically feature a slot-based design and may be replaceable. CPO modules are permanent and cannot be serviced in the field.

7.4.Q:What is the fundamental difference between XPO, NPO, and CPO?

A:The difference as following:

XPO: Front-panel pluggable module with integrated liquid cooling

NPO: Located on a PCB near the ASIC, typically featuring a socket-based design

CPO: Permanently integrated within the ASIC package

7.5.Q:When will XPO modules be commercially available?

A:A prototype of the XPO module is being demonstrated at the 2026 OFC conference (March 2026). With increased production capacity, commercialization is expected to be achieved between 2026 and 2027.

7.6.Q:Will CPO eventually replace pluggable optical modul?

A:That is not entirely the case. Different technologies will be suitable for different applications. Industry analysis indicates that removable optical engines (including XPO and NPO) will continue to account for the majority of the market share by the end of this decade.

7.7.Q: How does Google's architecture affect optical demand?

A:Google’s Ironwood TPU, combined with 3D Torus and Apollo OCS technologies, is creating significant demand for high-speed optical modules. TrendForce forecasts that by 2026, 4 million TPUs will drive more than 6 million high-speed optical modules.

7.8.Q: What is the outlook for Chinese optical module manufacturers?

A:Chinese manufacturers currently hold more than 70% of the global market share and dominate the high-speed electronics sector. Innolight ranks first globally, and seven of the top ten companies are Chinese. Given the scale of Chinese manufacturing and technological advancements, this leading position is expected to continue.